Leonardo Badea (BNR): Outlook for the coming year and possible responses to existing challenges

“In recent years, economies around the world have gone through a difficult and complicated situation, marked by the materialization of new global risks that have affected economic development and triggered transformations with long-term effects that will continue to represent a challenge for the conduct of economic policies during the next year as well.

It is therefore reasonable to assume that the many overlapping crises that influenced the economic evolution in 2022 will most likely shape the economic perspective of the next year, but in new forms and manifestations. The end of winter in the northern hemisphere (which hosts about 87% of the planet’s population) will find us at a moment of decisive choices regarding the adaptation to the new economic conditions generated by the effects of these crises. Therefore, we must continue to analyze how we can make adjustments to the economic and institutional environment at the global level to optimize the process of adaptation and transformation and reduce the negative impact on the economy and society.

In this sense, we have two alternatives, the first would be to target the problems we are aware of at the moment, in the short and medium term depending on the size of the induced risks; the second approach would be to do more than that and try to increase the resilience of systems, including in the face of risks that have not yet materialized but are possible in the medium or long term.

If we look at the immediate landscape we notice that at this moment the energy crisis, the conflict in Ukraine, delays and problems in supply chains, inflation, the COVID-19 pandemic draw the contours of a new year that will begin under the auspices of uncertainty. The effects of the COVID-19 pandemic seem to be fading, at least in Europe and the US, but there is still an impact that manifests itself in supply constraints for many categories of goods, and at the same time the prospect of pressure on the health system cannot be ignored, especially in the first part of the year, as long as the cold season continues, which is even usually marked by seasonal epidemic outbreaks.

The energy crisis is in full swing, and the impact of the conflict in Ukraine has revealed the major vulnerabilities of Europe, especially the dependence on Russian gas, and has determined the entry into a new paradigm, of the need to find alternative solutions, especially in the area of renewable energy, but also in the sense of increasing the efficiency and ensuring the energy security of the states.

Beyond the impact on the energy sector, the conflict in Ukraine (the end of which does not seem predictable at the moment) has accentuated already existing dysfunctions in the production and distribution chains, generated new supply difficulties especially for agri-food products, potentiated inflationary pressures, and contributed significantly to increased consumer and investor uncertainty.

The recent crises overlap with systemic challenges that existed before the COVID-19 pandemic but were overshadowed by it and the conflict in Ukraine, namely climate change and population aging in developed countries, both of which are vulnerabilities with deep negative impacts and no rapid and efficient solutions.

Analyzing the economic recovery in 2021, we conclude that it has been fragile and uneven, although there have been extensive support programs at national and international levels. In 2022, the global economy was marked by a slowdown, and the outlook for 2023 is for a reduction to 2.7% (according to IMF estimates – World Economic Outlook, October 2022), representing practically the weakest growth of the last two decades. The outlook for inflation is more optimistic, however, marking a decline from 8.8% in 2022 to 6.5% in 2023 (according to the aforementioned report).

In the eurozone, due to the impact of the energy crisis on prices and consumption, many economists expect a slight contraction of the economy next year and the continuation of actions to reduce inflation, which will remain above the European Central Bank’s target of 2% in 2023 as well. At the same time, it is worth noting the low level of the unemployment rate, at a record low of 6.6% (according to the estimates of the investment bank Morgan Stanley published in November 2022).

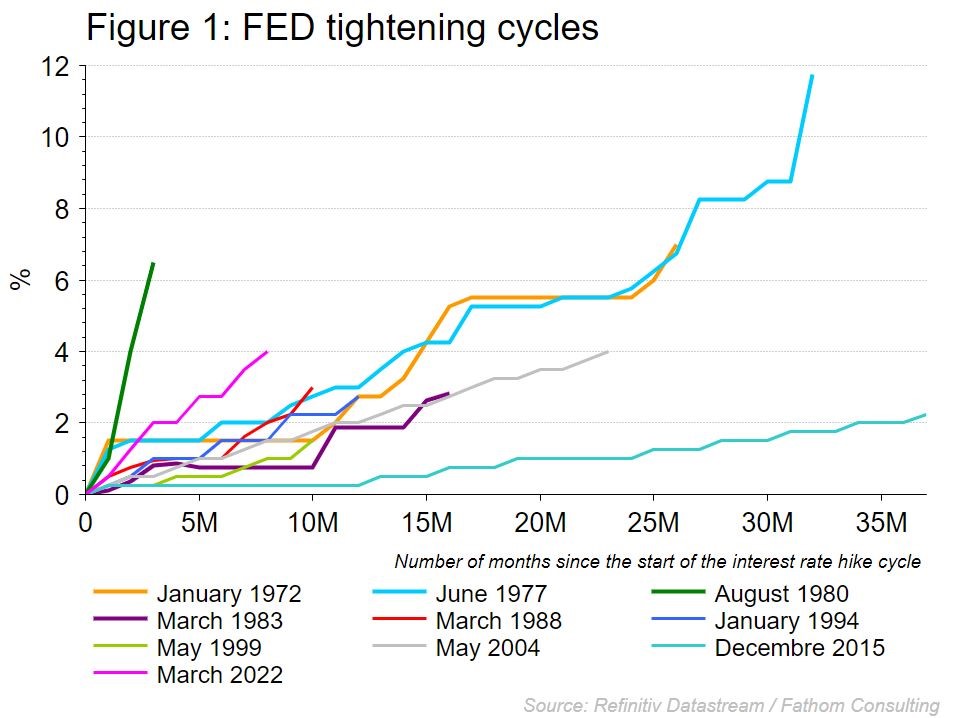

The year 2022 also marked the end of a relatively long period of “easy money” in the context of a reduced level of inflation in developed economies and implicitly accommodative monetary policies in previous years. Both the European Central Bank and the US Federal Reserve entered into an accelerated cycle of interest rate hikes in the latter part of the current year. In the US, the current cycle of key interest rate hikes is to date the second fastest in history (Figure 1), after the one that began in August 1980, during the tenure of Fed Chairman Paul Volcker.

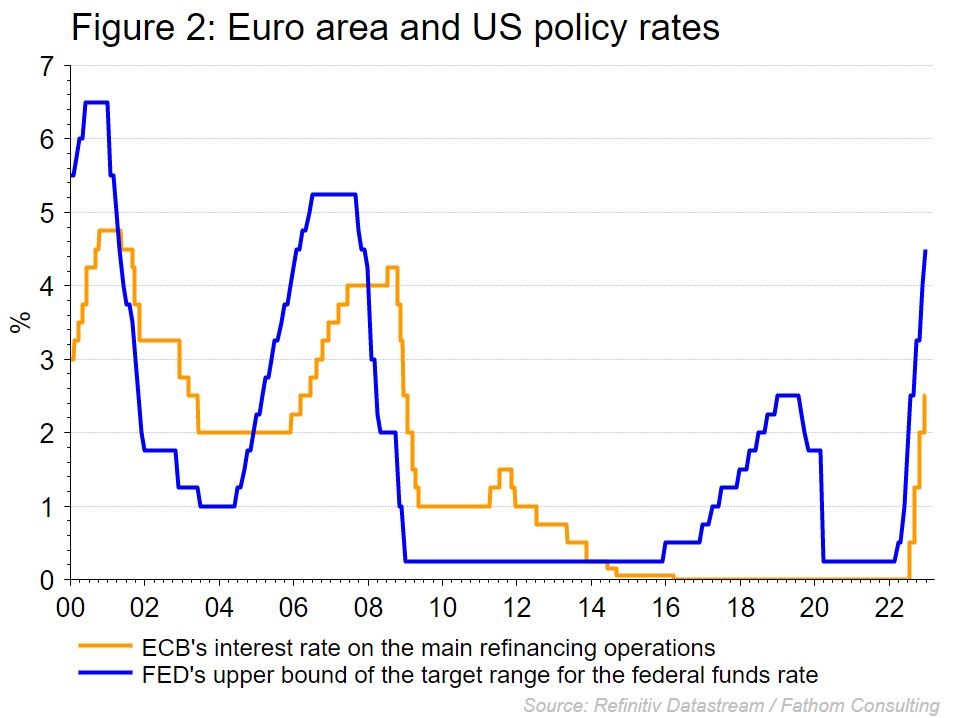

The recent increases in the monetary policy interest rates decided in December by the ECB and the FED led to their positioning at the highest levels since 2008-2009 and until now (Figure 2). Taking into account the official positions expressed, it is foreseeable that in the first part of next year the cost of financing in the two important currencies of international circulation will continue to increase, which will contribute to further reducing the accommodative character of monetary conditions at the global level, with restrictive effects on economic growth. There are expectations for European economies to contract, while emerging economies will experience a modest recovery; at the same time, forecasts for the economic evolution of Asia are more optimistic.

Given the association between inflation dynamics (still high) and unemployment (currently low in most economies), in the new year efforts will simultaneously focus on significantly tempering the price advance and avoiding a recession to lessen the negative effects of the reduction in economic dynamics on jobs.

Fiscally, given the current context and outlook for energy costs, priority of governments will naturally be vulnerable citizens, so we can anticipate continued support measures, at least for the foreseeable future. However, because the fiscal space is limited, and in some economies the need for fiscal consolidation is becoming increasingly pressing, the support measures will have to become prioritized towards the most vulnerable segments of the population and towards the strategic sectors of activity.

Also, public investment expenditures will have to be channeled towards the development and modernization of infrastructure, which would help both to increase economic efficiency and the development of many branches of activity in the private sector, at the level of the entire country, but also to progress towards the important objectives regarding the reduction of climate and energy crises effects. The growing pressure exerted by the effects of these two crises will leave no room for hesitation. All the messages and conclusions expressed following the COP27 that took place in November 2022 gained the emphasis of an ultimatum regarding the necessary actions in the field of the climate crisis.

The climate risks are doubled by the geopolitical ones, the fragility of the balance being revealed by the conflict in Ukraine, but also by the unstable perspective regarding developments in other areas, such as Taiwan, for example.

We therefore see that it is unlikely that geopolitical tensions will subside in the near future, as they are present in various forms and manifestations not only in the Russia-Ukraine area but also in the Middle East, large portions of Asia, and South America.

In this context, it is difficult to believe that a return to an easy situation from the perspective of international economic exchanges and to the stability of long value chains in the supply and production circuits of goods is possible. This is why, it is reasonable to assume that pressures on output and final prices will remain high for some time, supply-side syncopes will persist, and the importance of private and public investment to create/facilitate local and regional alternatives will become more and more obvious.

However, the equation is all the more complicated as the cost of financing/capital is very important to stimulate these investments, but it will not decrease as long as global inflation remains high, while inflation, even if it decreases, it is difficult to return to the very low levels before the current overlapping crises until the structural causes of the supply-side syncopes are removed.

We are therefore, unfortunately, in a vicious circle that can only be broken through innovative solutions combined with a lot of balance and moderation in the allocation of the limited resources currently available and with the prudent and efficient management of the existing room for maneuver for fiscal and monetary policies.

From a strategic point of view, some possible solutions for the future could be grouped in five important directions:

- Investment stimulation. At this moment there is a great need for investments arising from the need to transform the energy production and utilization model. Given the high level of prices throughout the production and distribution chain, there is potential for these investments to generate significant long-term returns, so they represent an opportunity for private finance capital, even in such a period of high interest rates. For their channeling, however, greater accessibility and simplicity of the administrative and regulatory framework is needed, which I am convinced is possible to achieve without in any way affecting fairness, fiscal rigor, and equal opportunities (level playing field). They can drive more efficient, cleaner, and inclusive economic growth and create additional opportunities in the private sector, along with many other significant additional benefits.

- Stimulating the process of research/innovation and adaptation of systems. Much of the fundamental structural change required consists in the transformation of key systems for the organization of production, transport, communications, etc. We are on the threshold of new changes regarding the functioning of cities and their development. New objectives are emerging regarding increasing the quality of life in urban communities, reducing pollution, and developing a circular economy. Let’s not forget that including on the labor market, the effects of the pandemic have brought deep, structural changes, the evolution of which is probably only at the beginning. We still do not know how they could influence future productivity, the quality of work results, social relations as a whole. But it is certain that all of these require combinations of institutional change, standards and regulations, design and appropriate policies. Systematically, over the long term, allocating greater resources to research and innovation activities will lead to the solutions and technologies that enable us to adapt to the challenges we face today. That is why, similar to the point above, we need the flexibility of administrative mechanisms and the adaptation of the legislative framework in order to facilitate, stimulate and protect research/innovation activities. The race for technology is now at least on a par with that for natural resources, with the effects on economic development being just as important.

- Continuation of global and regional funding programs and mechanisms aimed at strengthening the resilience of local economies, increasing cohesion and convergence, and combating inequalities. The aggravation of geo-political frictions in the last period, together with the increase of social tensions, are to an important extent determined by the accentuation of inequalities, both at the inter-state level and in the structure of society. There are many factors that have contributed to this deterioration of relations and growing discontent at all levels, among which economic and financial factors play an important role. In their case, a re-emphasis on global economic and financial cohesion and convergence policies would be beneficial for all involved, from multiple perspectives. The role of multilateral financing programs and mechanisms is a significant one, therefore they must be continued and developed. While many advanced economies have fiscal space or borrowing capacity, emerging and poor countries entered the most recent crises with high debt and limited resources. Domestic resource mobilization will need to contribute to incremental funding. But international financial collaboration will be critical.

- Improving business financing methods. The economies of many states tend to become overly dominated by large international conglomerates that have the ability to place themselves in a favorable fiscal and regulatory position by gaining more and more market share at the expense of local businesses. But experience has shown that for social well-being as well as for economic and financial stability, the role of small and medium-sized enterprises is at least as important as that of large international corporations. That is why competitive, fair, and compatible means with free market mechanisms must be found to stop the decline of local businesses and bring them back to the front-line place they deserve. From this perspective, access to financing under competitive conditions is crucial. Facilitating access to the recent new financing mechanisms created at the international level, such as crowdfunding, is an opportunity from this point of view. To these must be added a more important role of all segments of the capital market, especially those intended for medium-sized companies, start-ups, or business projects.

- Digital transformation. Global investment in digital transformation is expected to grow at a compounded rate of 17.1% per year, according to International Data Corporation, reaching $2.3 trillion by 2023. The largest players in the digital transformation space will continue to be The United States, followed by Europe and China, but worryingly, projections indicate a high probability that China will overtake Europe in this perspective by the end of next year. Artificial intelligence and applications based on machine learning will play an increasingly important role in the economy and could revolutionize the organization of production, inventory management, product and market strategies, etc. According to a recent report published by the consultancy and management company Accenture, technologies based on artificial intelligence could bring up to 40% increases in productive activities by 2035. Digital transformation will not only involve an advance in technology, but will have significant implications on the labor market and society as a whole, because people are the most important enabler of digital transformation.

A positive consequence of the situation in recent years is represented by the integration of digital technology in all aspects of social life and the acceleration of digitalization in many sectors, with an impact on consumers and business models, and this trend will continue to manifest itself in the year that is about to start. A series of trends will mark the evolution of the system in the future, and the preparation to respond to the demands is essential: we can estimate an increased demand for digitalized financial services, the continuation of the concern for increasing financial inclusion, a greater need to save and protect savings, a higher adaptability of services even up to the point of personalization according to the needs of individual consumers, changes in the client-bank relationship (by intensifying online interaction), an emphasis on consumer satisfaction, the focus on increasing security in use. If we look to the more distant future, it becomes obvious that uncertainty and high risks require flexibility and the adoption of innovative thinking (outside the box), being quite clear that the reality we knew in the pre-pandemic period cannot be recovered. The new year will therefore begin under the sign of a realignment building upon the call for adaptability while accepting uncertainty as a constant that we must manage and take into account”.